A Tale of Two Hats redux

I’ve written about the concept of two hats before. The idea is this: when you think about current economic issues, you can wear either of two hats, a Consumer Hat or an Investor Hat. Things you may not like as consumers, such as rising prices, flat wages, and the like, sometimes create positive opportunities in financial markets, when you wear your Investor Hat. But if you wear your Consumer Hat to make Investor-Hat decisions, you may make poor decisions, and reaching your financial goals may prove more difficult.

When I wrote about the two-hats concept, in 2008, strong winds were buffeting both hats. In many ways, we are in a similar situation right now. Let’s see how the two hats fit and function for you in 2011.

Inflation

Consumer Hat: With the overall rate of inflation comparatively low right now, as a consumer you haven’t had to pay increasing prices for most goods and services (that is, unless you eat, drive, or heat). One-and-a-half cheers for low inflation. Let’s hope it lasts, but I am not counting on it. Theoretically, in a low-inflation environment you should have money to spend or save for the future. (The “buts” are coming.)

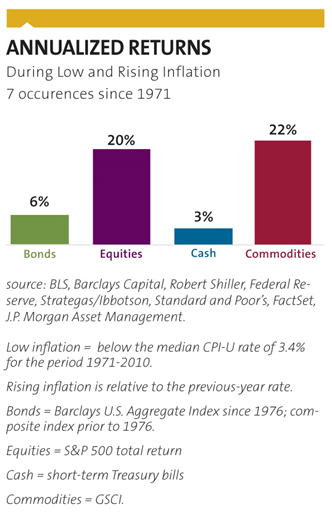

Investor Hat: Certain investments, such as bonds, often thrive in a low- or falling-inflation environment. But as an investor you must look ahead, not just back. Will inflation stay low in the future? Not likely, given growing global demand, high government deficits, and other factors. That changes the decision equations. Rising inflation, is tough on most bonds and long-term CDs, though inflation-protected Treasuries (TIPS) can be an exception. Commodities, precious metals, and stocks typically handle rising inflation better. The graph below shows the returns from four categories of investments in the seven periods of low and rising inflation that have occurred since 1971.

Rising Food and Fuel Prices

Consumer Hat: In the past year the price of gasoline has risen 98 cents (23% in 2011 alone). Many wholesale “producer” prices have risen even more: cotton, selling for 80 cents per pound a year ago now costs $2; and corn futures prices have doubled in the last year. Just these three items—gas, cotton and corn—have contributed to Southwest Airlines raising fares six times in 90 days, a Brooks Brother’s non-iron dress shirt going from $69 to $88, and Doritos chips coming in bags 20% smaller. These are another side to the “low-inflation” coin. Keep in mind, federal government reports on inflation focus on “core inflation,” which excludes energy and food prices. “What?” you say? You heard right, two of the basic costs of daily life are largely ignored in the reported inflation rates. There are reasons for the omission, but the fact remains, as we spend more on driving, eating and clothing, our ability to put our money to other uses diminishes. And with that, the potential for a stalled economy looms. Economists estimate that every $10 increase in the price of a barrel of oil reduces economic growth by 0.2%. In an economy that is now only growing at an estimated 1.5% – 2.0%, that has an impact.

Investor Hat: This energy and food inflation puts the emphasis on a few key factors, some event-driven, others policy-driven. The event-driven ones include non-ideal weather in the past growing season, surging demand in emerging foreign markets, and political unrest overseas. The policy-driven factors include farming subsidies, restrictions on domestic energy production, and monetary policy, to name a few. In regard to the last one, the Federal Reserve is tasked with assuring low inflation and low unemployment. It is operating on the belief that it can keep interest rates low now to boost employment, but can increase them in time to stave off core inflation. This has not been easy to do in the past, nor has it often been done successfully. Given these factors, how do you see your opportunities while wearing your investor hat? When inflation is accelerating, equities, commodities, and precious metals perform better than cash and bonds. (In the case of cash, each dollar is worth less as more are in circulation; in the case of bonds, the debt is paid back to you with dollars that are worth less.)

Weakened U.S. Dollar

Consumer Hat: The dollar weakened in value as the Federal Reserve increased the money supply (twice) to help our faltering economy. To us consumers a weak dollar means foreign goods and trips to foreign countries cost more (and you’ve noticed that foreign goods are a large proportion of your purchases). The issue is more complex with oil (and gasoline) prices. Oil is priced in dollars; so when the dollar weakens, oil producers raise prices to offset the lower value of their revenues. We, the consumers, feel the pinch. When a weaker dollar is coupled with increased demand for oil around the world, prices can get truly ugly. ($5 a gallon by summer? A possibility.)

Investor Hat: When we look at investments, again we must remove our Consumer Hat. Certain investments perform better with a weak dollar. These include investments that have positions in foreign currencies. Your return from investments in your portfolio that include Japanese yen, the U.K.’s pound, even the euro, has probably been favorable. Other investment possibilities include gold and precious metals, emerging markets, securities, bonds, and foreign equities. But keep in mind that renewed economic growth in the U.S., coupled with turmoil elsewhere, could halt or even reverse, the dollar’s fall.

Economic Recovery

Consumer Hat: Most observers agree that the current economic recovery is fragile rather than robust. By government measurements we have been out of a recession for almost two years. But, boy it doesn’t feel that way to many. Unemployment stays stubbornly high, especially factoring in those who are no longer looking. Some industries and companies appear very busy, while others are stagnant. Raises and bonuses have reached some, while others still worry about retaining employment each day. Due to this, consumer sentiment measures read quite low. Though spending has picked up on household needs, vacations, and other discretionary needs, there is a mood in the air that the recovery is not “real” or long lasting. If you match to this type of thinking, your best bet as a consumer is to be ultra prudent, save more, reduce debt, and give yourself a “margin for error.”

Investor Hat: An investor must think differently. A nascent, still-uncertain global recovery presents opportunities for growth as well as reversal. Precious metals, Treasury bonds, and utility stocks frequently offer protection in economic swoons. But commodities, “growth” stocks, emerging-market stocks, even real estate, do better in periods of economic growth. Small-company stocks, with their higher risk, frequently have the greatest gains in the early stages of an economic recovery. Yet large, high-quality multi-national corporations typically have the resources and capabilities to capitalize on economic growth, along with the financial strength to survive a global or U.S. economic reversal. In any case, uncertain conditions call for particular attention to balance and diversity.

None of the possibilities I’ve been mentioning is based on timing the market. My colleague Jack Kraus, Allegheny’s Chief Investment Officer, notes that people usually only keep in mind ‘known threats’ to their portfolio, but that it is usually the ‘unknown threats’ that leave in investors most vulnerable to portfolio damage. Threats can come from omissions as well as inclusions. You may already have many of the investments I’ve been mentioning. But the list of possibilities may allow you to broaden your investment selections in a prudent way. Part of prudence is remembering that money put in the stock market should be aimed at achieving long-term objectives, those at least five years ahead.

The two-hat perspective on financial decisions reminds us not to throw in the investment towel, or hatband, during a period of slow economic growth, high fiscal challenges to the country, energy conflicts, and an uncertain political climate.

Author: David Jeter, CFP®, Allegheny Financial Group, April 2011

Securities offered through Allegheny Investments, LTD, a registered broker/dealer. Member FINRA/SIPC.

The above comments are provided for discussion purposes only and are not meant to be an offer of any specific investment.