Family Matters: Getting Your Financial House in Order

Not too long ago, I signed up for the new marriage, new house, and newborn extravaganza. As many of you know, and I can certainly attest to now, it is quite the transition. Times were a bit simpler before—pay your rent, go to work, brush your teeth at least twice a day, and look generally presentable. You blink, and all of a sudden you’re saving for two, then three, all while juggling your career, raising a little one, being a thoughtful spouse, paying real estate taxes, and worrying about the overall health of your lawn. My wife may not share that last sentiment...

It has been the most exciting, joyous, and fulfilling time of my life. That said, even as a financial planner, it hasn’t been without its nagging thoughts: Am I saving enough? Am I taking advantage of my benefits through work? Should I be thinking about saving for college already? Would my family be okay (financially) if something terrible happened to me? Should I have an estate plan in place? What the heck is a Bumbo?

Although a lot of these issues are uncomfortable to discuss and an added expense during an already expensive time, handling them now will not only give you peace of mind but a solid foundation for securing your family’s financial future.

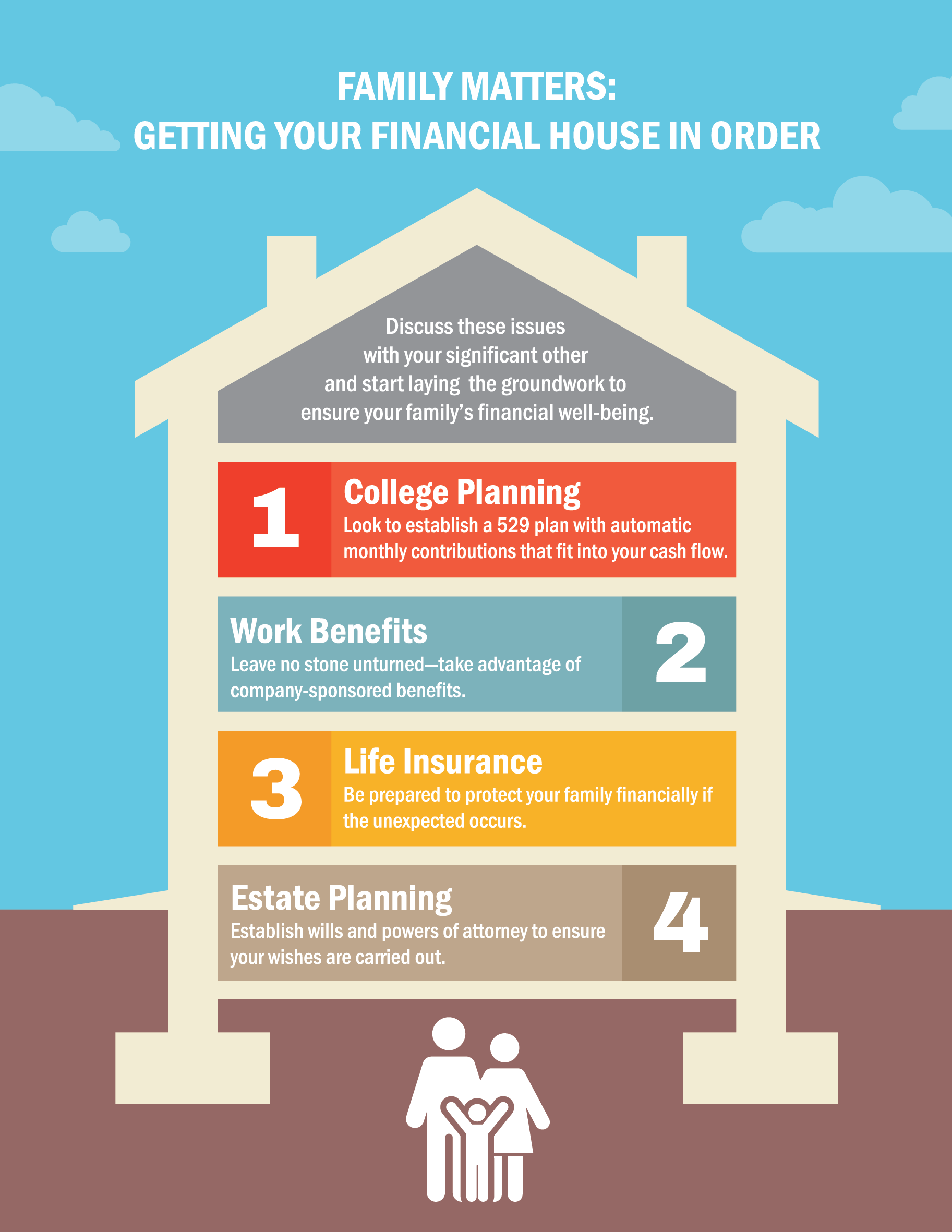

College Planning

As you know, college is already an (almost illogically) expensive journey. That, however, is not slowing the majority of private colleges from increasing tuition year after year. If it’s your family’s wish to help cover some or all of these costs, start saving when they’re in diapers. The earlier, the better.

Look to establish a 529 plan and set up an automatic monthly contribution for an amount that fits into your cash flow. You won’t even notice it after a few months. Also, let the grandparents know. They just may want to lend a hand.

Work Benefits

Although there are many and they will differ from company to company, I wanted to highlight one in particular—the Dependent Care Flexible Spending Account. This account allows the parent to set aside income before taxes in order to help pay for the costs of childcare. Depending on your tax bracket, this can easily save you 20 to 30% on what you elect to contribute.

Life Insurance

The focus of life insurance is to cover a period of time in which your family is financially vulnerable. This window of liability typically exists during your working years. Once you’ve reached retirement, you’re no longer relying on wages to sustain your family’s lifestyle. From that mindset, term life insurance is truly the most effective (and cheapest!) way to go.

So how do you know how much to purchase? If you’re not running a thorough analysis on your existing portfolio, anticipated growth, and future cash flow, a good rule of thumb is 10x salary. Have a qualified adviser go out to bid to find a reputable insurance company that will provide that coverage at the most cost-effective rate. If you’re not in good health, if you smoke, or have a family history of heart disease, for instance, the low-cost alternative may be to obtain that level of coverage through your employer. They will likely offer guaranteed coverage at group rates for up to some multiple of salary.

Estate Planning

This is an important one. And likely the one issue on this list that most young families ignore. Contact an estate attorney and establish wills and powers of attorney. Although this may set you back several hundred dollars, thankfully it can be a one-time cost.

In an ideal world, these documents will collect dust and remain untouched until your late 80s or 90s. The unfortunate reality is that sometimes bad things happen. Spelling out guardianship for a minor child or enlisting a friend or family member to make financial or healthcare decisions on your behalf, is a critical element to ensuring your wishes are carried out.

Also, be sure to update the beneficiary elections on your various retirement plans and life insurance policies. The election you make on these will trump anything your will spells out. So confirm that these are working in concert with one another.

Final Thoughts

I know this conversation can easily be placed on the backburner as it tends to make certain individuals anxious and stressed. Try not to be deterred. Set aside some time to discuss these issues with your significant other and start laying the groundwork to ensure your family’s financial well-being. Consider hiring a CERTIFIED FINANCIAL PLANNERTM to help you along the way – and outsource a headache.

And for those still wondering, it turns out that a Bumbo is a foam chair that helps your baby sit upright. Who knew?

Author: Matthew D. Kelly, CFP® | Financial Advisor | Allegheny Financial Group | May 2017

Allegheny Financial Group is a Registered Investment Advisor. Securities offered through Allegheny Investments, LTD, a registered broker/dealer. Member FINRA/SIPC.

Share This Story, Choose Your Platform!