Key Steps to Combat the Rising Cost of a College Education

It is no secret that a college education is expensive. Between tuition, fees, room and board, the total cost can be mind boggling for parents that have not paid attention to the cost of tuition since they graduated decades before.

That being said, as expensive as college is, it is still often the best investment anyone can make, and it sets the stage for a successful and productive career. The key to preparing for this large, but necessary expense is developing a plan early and sticking with it. A successful plan will estimate the future cost of the child’s education; utilize tax-advantaged plans such as a 529 Savings Plan; and develop a monthly or yearly savings plan to meet that goal. Here are questions we are often asked by clients when helping them develop a college savings plan:

It seems like college is a lot more expensive than it used to be. Is that really the case, or is that just because of inflation?

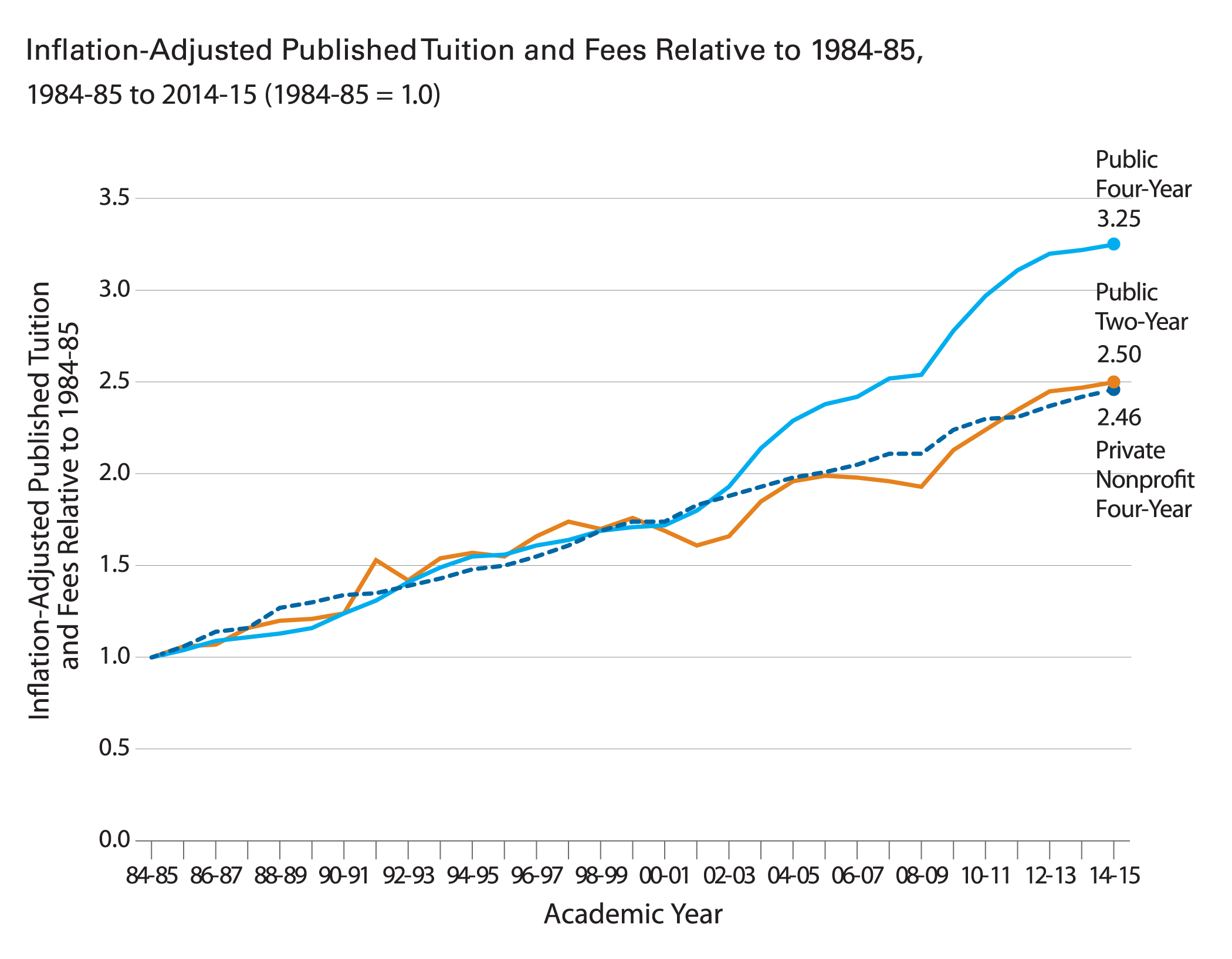

While it’s clear a college education is necessary for most people, affording it is becoming increasingly difficult. Published tuition prices are increasing at a greater rate than inflation, and have been doing so for over 30 years (see Figure 1). Today, an education at an average Four-Year Private college would total $169,6761.1 That sounds like a big number, however assuming college costs continue to increase at a rate of around 6%, someone born today will have to pay $529,670 for that same education.

Figure 1

Source: The College Board, Trends in College Pricing 2014, Figure 6.

Can college costs really continue to double inflation?

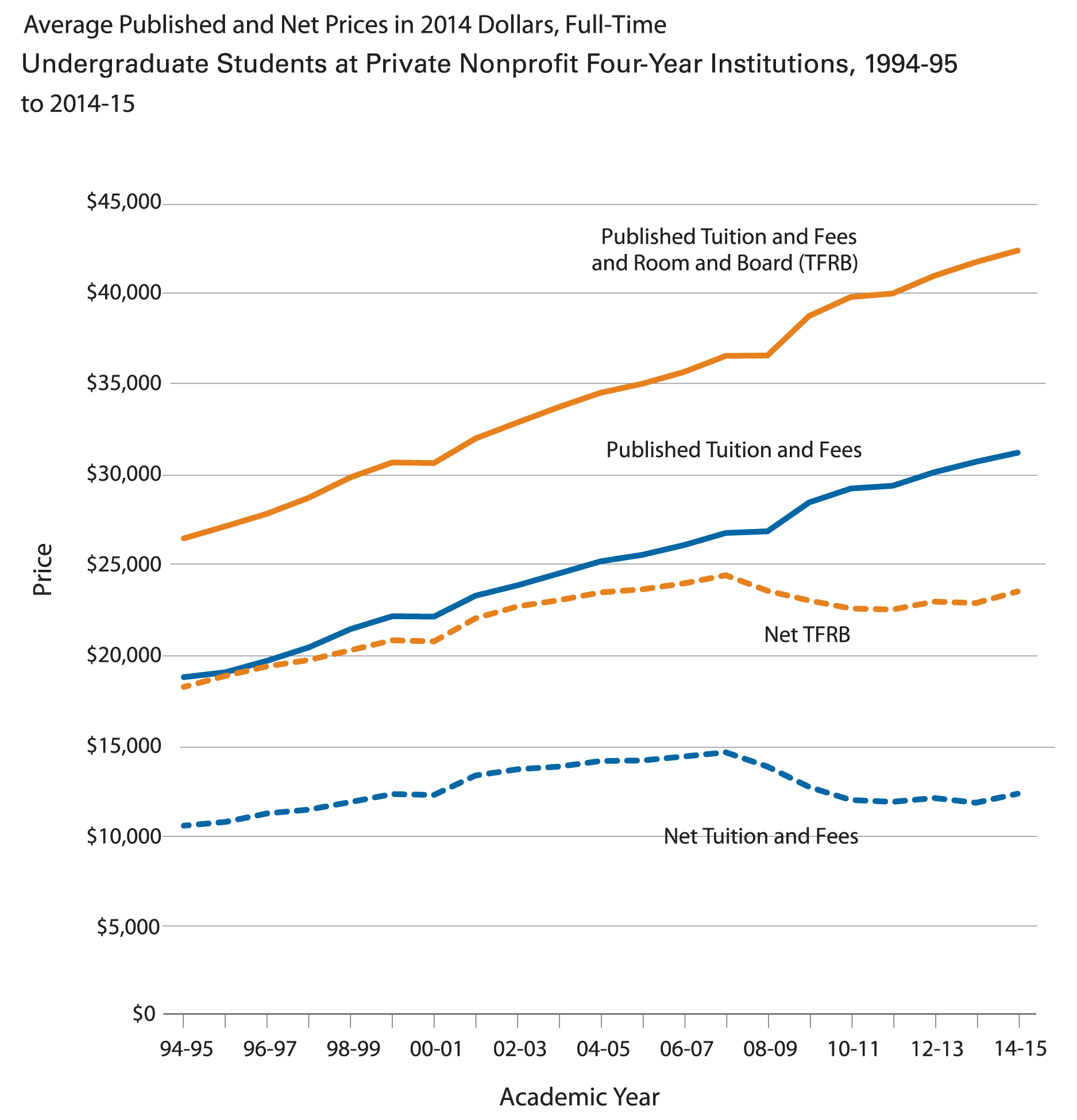

That largely depends on your household income and what a formula says you can afford. Colleges use financial aid to make college “affordable” for those from varied economic backgrounds. They determine the amount of financial aid by using a formula which looks at the income of parents and number of children in the household to determine how much the family can afford to contribute, known as the Expected Family Contribution (EFC). As illustrated in Figure 2, the “Published Cost” of attending an average four year college continues to rise, but the “Net Cost” (after financial aid) has largely remained the same over the past 20 years, even decreasing in some cases. It is important to recognize whether you are likely to receive financial aid, and if you’re not, planning for the future cost becomes even more important.

Figure 2

Source: The College Board, Trends in College Pricing 2014, Figure 13.

Based on figures for the 2014-2015 school year, a student attending an average four-year public college coming from a family of four would be eligible for financial aid only if their parents made less than $140,0002 per year. Those coming from families that made in excess of $140,000 would be ineligible for aid and would be responsible for the full cost of attendance.

So to answer the question of whether costs will continue to double inflation, the answer largely comes down to, how much do you make? If you make enough, the answer is yes, and you better start preparing to cover that cost now.

What is the best way to save for college?

A popular vehicle for college savings is a 529 Plan. These tax-advantaged accounts are specifically designed for saving for education costs. Contributions grow tax-deferred and are distributed without any tax impact as long as the funds are used for qualified education expenses. Each plan has different investment options, but most offer the ability to invest in a menu of mutual funds which can give the account exposure to both the bond and equity markets. As a bonus, many states (including Pennsylvania) offer a state tax deduction for 529 plan contributions.

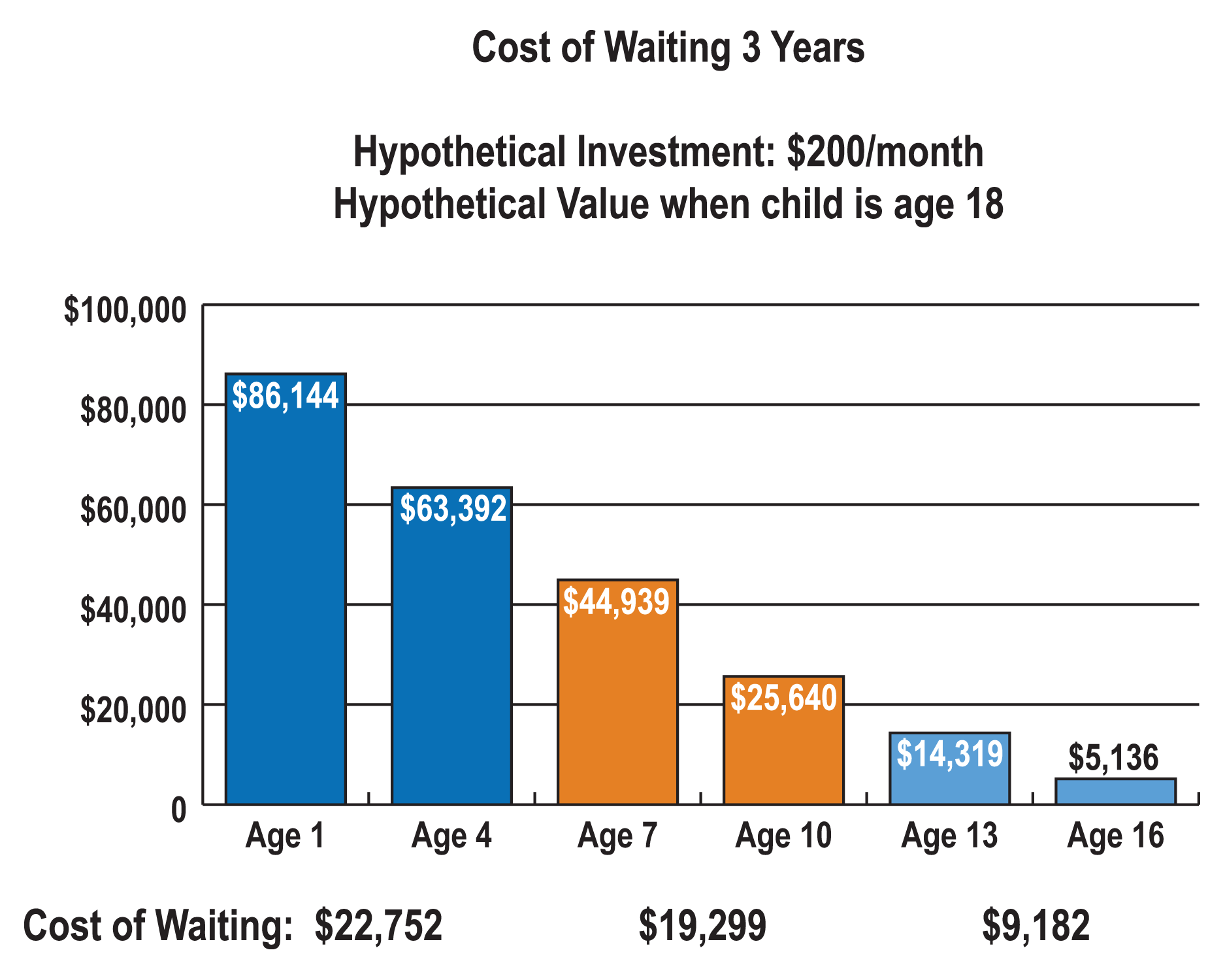

The key to saving for college is no different than saving for any other long-term goal: time. Recognizing the importance of the time value of money and taking advantage of the power of compounding can have a dramatic effect on your ability to fund future education expenses, as shown in Figure 3.

Figure 3

This chart is for illustrative purposes only, does not represent any particular investment, and does not include transaction fees or taxes. These estimates assume a contribution of $200/month and a 7% average annualized rate of return compounded monthly.

Source: Ingram, Leah. “May 29 Is 529 Plan Day.” Suddenly Frugal. 28 May 2014.

The first step in successfully funding your child’s education is recognizing that the time to start saving is now. The next step is determining what investment options to choose and how much you need to save each month. The answers to these questions vary widely for each individual situation, and are often best answered with the help of a qualified Financial Advisor who can guide you through the process and develop a personalized plan based on your goals.

1 The College Board, Trends in College Pricing 2014, Table 1A. 2Onink, Troy. “2015 Guide To FAFSA, CSS Profile, College Financial Aid And Expected Family Contribution (EFC).” Forbes.com, 28 Nov. 2014.

Securities offered through Allegheny Investments, LTD, a registered broker/dealer. Member FINRA/SIPC. The above comments are provided for discussion purposes only and are not meant to be an offer of any specific investment.

Share This Story, Choose Your Platform!