Inheriting an IRA or Roth from a spouse comes with its own set of rules and key deadlines. If you inherit an IRA or Roth from a spouse, you can combine that IRA or Roth with your own, or you can roll the IRA to an inherited IRA or disclaim the assets altogether.

Roll into your own IRA

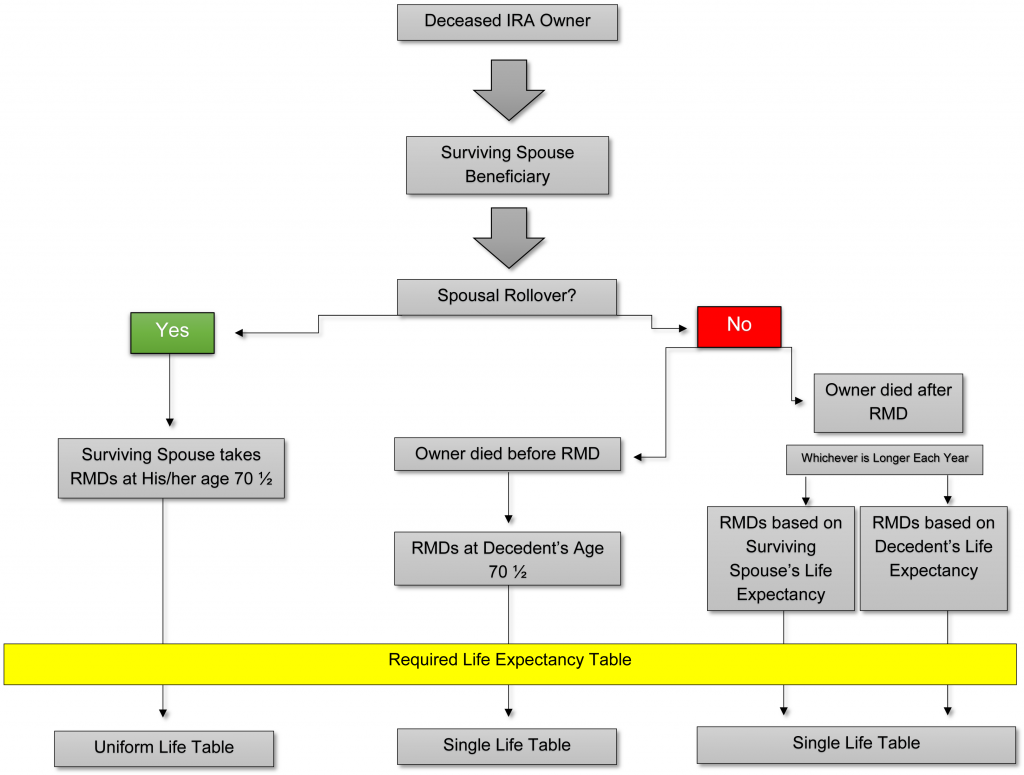

If the surviving spouse decides to roll the IRA into their own, distributions will start when they have attained age 70 ½ and are based on their own life expectancy using the Standard Uniform Life Table. Although the surviving spouse can delay distributions until age 70 ½, they cannot take distributions before age 59 ½ without a penalty. Non-spouse beneficiaries do not have the luxury of being able to roll the inherited IRA into their own IRA.

Treat as an inherited IRA

If the surviving spouse chooses to treat the IRA as an inherited IRA, any money withdrawn from the inherited account will not be subject to the 10% early withdrawal penalty. This may be beneficial for young spouses by providing flexibility if the surviving spouse may need cash flow.

The good news is that there is no deadline on when a spousal rollover must occur, and it is possible to do a rollover years after the surviving spouse initially inherits the account. The younger spouse could simply leave the account as an inherited IRA until reaching age 59 ½ and then roll the account over to their own IRA once the withdrawal penalty no longer applies.

Inherited IRAs have a specific set of rules when it comes to distributions. If the deceased spouse was over age 70 ½ and was taking distributions, those distributions need to be satisfied. A Roth IRA does not require minimum distributions if the surviving spouse rolls the Roth into their own Roth. If a spouse inherits a Roth IRA, they are required to take required distributions when the deceased spouse reaches age 70 1/2. Withdrawals made before age 59 ½ would avoid the 10% penalty on taxable earnings.

If a surviving spouse decides to treat the IRA as an inherited IRA, and the deceased spouse had not started required distributions, two options exist: 1) the entire balance is taken in full by the end of the fifth year following the year of death, or 2) minimum distributions will start at the decedents age 70 ½ but will use the spouse’s life expectancy recalculated each year using the single life expectancy tables (Table I of Appendix B in IRS Publication 590-B).

If the deceased spouse had started required distributions, distributions could be calculated two different ways. One calculation is based on the surviving spouse’s life expectancy recalculated. The other calculation is based on the decedent’s life expectancy reduced by one each year. The option that provides the longer payout should be used.

As shown in the illustration below, a surviving spouse has many options to consider when inheriting an IRA or Roth IRA from a spouse. Consult a financial adviser to help determine which choice is right for you.

Printer-Friendly PDF

Printer-Friendly PDF

Author: Nancy D. McKee, CFP® | Financial Advisor | Allegheny Financial Group | March 2018

Allegheny Financial Group is a Registered Investment Advisor. Securities offered through Allegheny Investments, LTD, a registered broker/dealer. Member FINRA/SIPC.