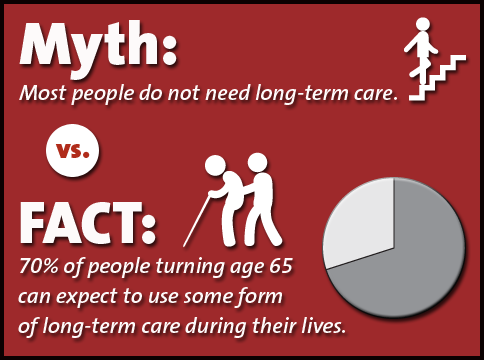

November is the ideal time to discuss long-term care with your financial advisor and learn how they can help you plan for a more secure future. At least 70% of people over the age of 65 will require some form of long-term care services and support during their lives.* If you are like most people, you aren’t thinking or talking about the financial and emotional aspects of long-term care needs. Long-term care is a range of services and supports you may require to meet personal care needs. Most long-term care is not medical care, but rather assistance with the basic personal tasks of everyday life, sometimes called Activities of Daily Living (ADLs), such as:

- Bathing

- Dressing

- Using the toilet

- Transferring (to and from bed or chair)

- Caring for incontinence

- Eating

Long-term care insurance can help:

- preserve savings and income

- maintain control about where care is received

- provide the ability to afford higher quality or greater frequency of care

- reduce dependence on government programs like Medicaid and Medicare

- relieve loved ones from the responsibility of caregiving.

*Source: Long-Term Care

Printer-Friendly PDF

Printer-Friendly PDF

Author: Barb Leson, FMLI | Insurance Director | Allegheny Financial Group | November 2015

Allegheny Financial Group is a Registered Investment Advisor. Securities offered through Allegheny Investments, LTD, a registered broker/dealer. Member FINRA/SIPC. The above comments are provided for discussion purposes only and are not meant to be an offer of any specific investment or tax advice.