September is Life Insurance Awareness Month (LIAM) and the perfect time to emphasize the importance of life insurance with your financial adviser. Life insurance is a simple answer to a very difficult question: How will my family manage financially when I die?

Benefits of Life Insurance

Benefits of Life Insurance

Life insurance can provide powerful benefits. For instance, life insurance proceeds can:

- Pay for funeral costs

- Help pay the bills and meet ongoing living expenses

- Pay outstanding debt

- Continue a family business

- Finance future needs such as your children’s education

- Protect a spouse’s retirement plans

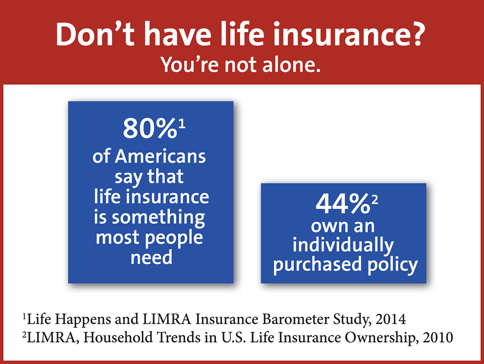

At the end of 2013, individual life insurance protection in the United States totaled $11.4 trillion dollars. While this seems like a large amount, in reality it amounts to less than $40,000 for each man, woman and child in the United States. Even worse, many do not even have that coverage, as more than 40% of Americans have no individual or group insurance coverage.

Types of Life Insurance

The basic feature of a life insurance policy is the death benefit which is the lump sum payment that your beneficiary will receive in the event of your death. The types of insurance are as follows:

Term insurance provides protection for a specific period Term insurance provides protection for a specific period of time (the “term”) and is for temporary circumstances, i.e. 10, 15, 20, 25, 30 years, etc. Term insurance offers the greatest amount of coverage for the lowest initial premium. There is no cash value with term insurance. However, the policy can also be converted to a permanent policy.

Permanent insurance offers protection for your lifetime and has cash value. Premiums are higher than term insurance. The types of permanent insurance are Whole Life, Universal Life, and Variable Universal Life.

How do you calculate how much life insurance you may need?

One way to answer this question is to determine the following:

- How much money will my family need after my death to meet immediate expenses such as funeral expenses, debts, taxes, medical bills, etc.? Plus,

- How much money will my family need to maintain their standard of living over the long run?

The best way to figure out the amount and type of life insurance that makes sense for your situation is to meet with your financial adviser and have a discussion to weigh your options.

Printer-Friendly PDF

Printer-Friendly PDF

Author: Barb Leson, FMLI | Insurance Director | Allegheny Financial Group | September 2015

Allegheny Financial Group is a Registered Investment Advisor. Securities offered through Allegheny Investments, LTD, a registered broker/dealer. Member FINRA/SIPC.

The above comments are provided for discussion purposes only and are not meant to be an offer of any specific investment or tax advice.