College Funding: How to Determine Your Expected Family Contribution

Applying to colleges is often a stressful time for both students and parents. During this time, families are asked to complete the Free Application for Federal Student Aid (FAFSA), which can be a daunting task.

The FAFSA helps calculate the Expected Family Contribution (EFC) that is used to determine financial aid eligibility. Many families are surprised to learn the EFC amount can vary greatly from the amount the family has available to pay for school.

What is the Expected Family Contribution (EFC)?

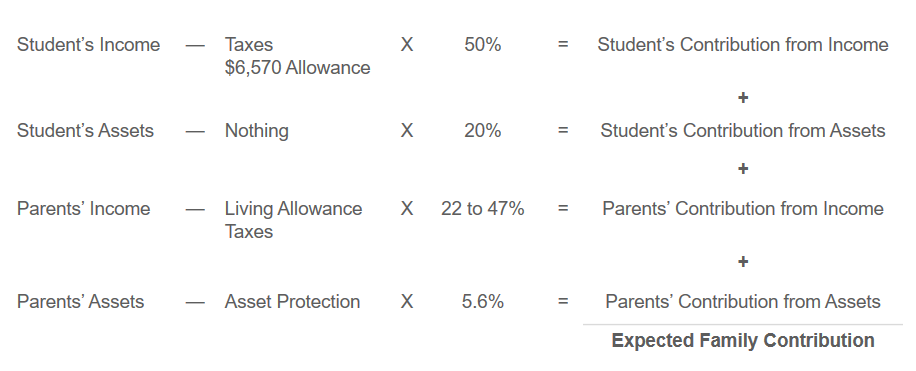

It is important to know that the Expected Family Contribution is not the amount the student will pay, nor is it aid the student will receive. The student’s need is calculated by subtracting the EFC from the school’s cost of attendance. The Expected Family Contribution is calculated using a combination of the parents’ and child’s income and assets. The cost of attendance includes tuition and fees, room and board, books, supplies, transportation, loan fees, and child or dependent care.

How to Calculate EFC

Two methodologies used to calculate EFC are Federal and Institutional. The Federal methodology, published by the Department of Education, is the most common method used by schools. Both Federal and Institutional methods use a similar formula; however, they differ in weights assigned to income and assets. The Institutional methodology may also include additional assets, such as home equity. For this discussion, we will focus on the Federal methodology.

Income Types Used

The types of income used to calculate EFC include: earned income, dividends, capital gains, and retirement income. The parents’ income accounts for between 22% and 44%, while the student’s income is counted at 50%. However, there is a certain portion of income that is not counted toward the EFC. For students, $6,570 is excluded from income, and for parents, the exclusion amount varies based on the number of dependents and number of students in college.

How Assets Are Weighted

Both child and parental assets are also used for the EFC. Child assets are more heavily weighted, with 20% of the child’s assets used in the EFC. Conversely, only 2.6% to 5.64% of parents’ assets are assessed. While it may seem prudent to transfer the child’s assets to the parents upon entering college, there are outside factors to consider, such as tax consequences.

529 Plan Effects and Considerations

529 plans are a unique asset in the EFC calculation. Proper ownership of 529 plans can be beneficial because a 529 plan owned by a child is considered a parental asset. So, 529 plans receive favorable treatment if either the parent or child owns it. However, holding a 529 plan in someone else’s name, such as a grandparent, could adversely affect the calculation. While these assets are exempt from being reported before disbursement, they are counted as income once they are used for the student’s benefit. Unfortunately, disbursements are then considered student income, which has the least favorable rate for the EFC computation, compared to the parental asset rate. The same situation may apply to divorced spouses. If the 529 plan is not in the name of the parent who is filing the FAFSA, the distributions could be treated as income for the child, just as if a grandparent had held it.

Retirement Accounts

Qualified retirement accounts are also excluded from the EFC calculation. However, pre-tax contributions to qualified accounts are considered parental income.

How to Calculate Expected Family Contribution

Needs Analysis Formula

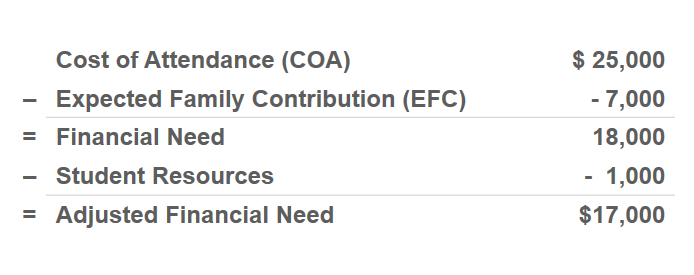

In conclusion, if the Expected Family Contribution is less than the school’s cost of attendance, the student qualifies for financial aid. Even so, financial aid may not come in the form of “free money.” The aid could be government student loans or work-study programs. Also, eligibility and amounts may vary by institution and year. The EFC is a complex computation with many variables. Your Allegheny Financial Group adviser can guide you through the financial aid process and help you determine the best college funding method for your family.

Author: Ben Grom, CFP® | Financial Planning Analyst | Allegheny Financial Group | November 2017

Allegheny Financial Group is a Registered Investment Advisor. Securities offered through Allegheny Investments, LTD, a registered broker/dealer. Member FINRA/SIPC.

The information included herein was obtained from sources which we believe reliable. This report is being provided for informational purposes only. It does not represent any specific investment and is not intended to be an offer of sale of any kind. Past performance is not a guarantee of future results.

Share This Story, Choose Your Platform!